Archive for category OSS data

Reliability of open source from a software engineering point of view

Posted by cdaffara in OSS business models, OSS data on April 6th, 2009

At the Philly ETE conference Michael Tiemann presented some interesting facts about open source quality, and in particular mentioned that open source software has an average defect density that is 50-150 times lower than proprietary software. As it stands, this statement is somewhat incorrect, and I would like to provide a small clarification of the context and the real values:

- First of all, the average that is mentioned by Michael is related to a small number of projects, in particular the Linux kernel, the Apache web server (and later the entire LAMP stack), and a small number of additional, “famous” projects. For all of these projects, the reality is that the defect density is substantially lower than that of comparable proprietary products. A very good article on this is Succi, Paulson, Eberlein. An Empirical Study of Open-Source and Closed-Source Software Products, IEEE TRANSACTIONS ON SOFTWARE ENGINEERING, V.30/4, april 2004, where the study was performed. It was not the only study on the subject, but all pointed at more or less the same results.

- Other than the software engineering community, some results from companies working in the code defect identification industry also published some results, like Reasoning Inc. A Quantitative Analysis of TCP/IP Implementations in Commercial Software and in the Linux Kernel, and How Open Source and Commercial Software Compare: Database Implementations in Commercial Software and in MySQL. All results confirm the much higher quality (in terms of defect per line of code) of the academic research.

- Additional research identified a common pattern: the initial quality of the source code is roughly the same for proprietary and open source, but the defect density decreases in a much faster way with open source. So, it’s not the fact that OSS coders are on average code wonders, but that the process itself creates more opportunity for defect resolution on average. As Succi et al. pointed out: “In terms of defects, our analysis finds that the changing rate or the functions modified as a percentage of the total functions is higher in open-source projects than in closed- source projects. This supports the hypothesis that defects may be found and fixed more quickly in open-source projects than in closed-source projects and may be an added benefit for using the open-source development model.” (emphasis mine).

I have a personal opinion on why this happens, and is really related to two different phenomenons:the first aspect is related to code reuse: the general modularity and great reuse of components is in fact helping developers, because instead of recoding something (introducing new bugs) the reuse of an already debugged component reduces the overall defect density. This aspect was found in other research groups focusing on reuse; for example in a work by Mohagheghi, Conradi, Killi and Schwarz called “An Empirical Study of Software Reuse vs. Defect-Density and Stability” (available here) we can find that reuse introduces a similar degree of improvement in the bug density and the trouble report numbers of code:

As it can be observed from the graph, code originated from reuse has a significant higher quality compared to traditional code, and the gap between the two grows with the size (as expected from basic probabilistic models of defect generation and discovery).

The second aspect is that the fact that bug data is public allows a “prioritization” and a better coordination of developers on triaging and in general fixing things. This explains why this faster improvement appears not only in code that is reused, but in newly generated code as well; the sum of the two effects explains the incredible difference in quality (50-150 times), higher than any previous effort like formal methods, automated code generation and so on. And this quality differential can only grow with time, leading to a long-term push for proprietary vendor to include more and more open source code inside of their own products to reduce the growing effort of bug isolation and fixing.

Dissecting words for fun and profit, or how to be a few years too late

Posted by cdaffara in OSS business models, OSS data, divertissements on April 3rd, 2009

So, after finishing a substantial part of our work on FLOSSMETRICS yesterday, I believe that I deserve some fun. And I cannot ask more than a new, flame-inducing post from a patent attorney, right here, that claims that open source will destroy the software industry, just waiting to be dissected and evaluated- he may be right, right? Actually, not; but as I have to rest somehow between my research duties with the Commission, I decided to prepare a response- after all, the writer is a fellow EE (electrical engineer), and so he will probably enjoy some response to his blog post.

Let’s start by stating that the idea that OSS will destroy the software industry is not new; after all, it is one of the top 5 myths from Navica, and while no-one tried to say that in front of me, I am sure that it was quite common, a few years ago. Along with the idea that software helps terrorists:

‘Now that foreign intelligence services and terrorists know that we plan to trust Linux to run some of our most advanced defense systems, we must expect them to deploy spies to infiltrate Linux. The risk is particularly acute since many Linux contributors are based in countries from which the U.S. would never purchase commercial defense software. Some Linux providers even outsource their development to China and Russia.’ (from Green Hills Software CEO, Dan O’Dowd).

So, let’s read and think about what Gene Quinn writes:

“It is difficult, if not completely impossible, to argue the fact that open source software solutions can reduce costs when compared with proprietary software solutions, so I can completely understand why companies and governments who are cash starved would at least consider making a switch, and who can fault them for actually making the switch.”

Nice beginning, quite common in debate strategy: first, concede something to the opponent. Then, use the opening to push something unrelated:

“The question I have is whether this is in the long term best interest of the computing/software industry. What is happening is that open source solutions are forcing down pricing and the race to zero is on.”

Here we take something that is acknowledge (that OSS solutions are reducing costs, thus creating a pressure on pricing) and then we attach a second, logically unconnected term: “the race to zero is on”. Who says that the reduction in pricing leads to a reduction to zero? No one with an economics background. The reality is that competition brings down prices, theoretically (in a perfectly competitive environment made of equal products) bringing the price down to the marginal cost of production. Which is, of course, not zero- as any software company will happily tell you. Because the cost of producing copies of software is very small, but the cost of creating, supporting, maintaining, documenting software is not zero. This does not take into account the fact that some software companies enjoy profit margins unheard of, and this explains why there is such a rush by users in at least experimenting with potentially cost-saving measures.

“as zero is approached, however, less and less money will be available to be made, proprietary software giants will long since gone belly-up and leading open source companies, such as Red Hat, will not be able to compete.“

Of course, since zero is not approached, the phrase is logically useless (what is the color of my boat? any as you like- as I don’t own one). But let’s split it in parts anyway: of course, if zero is approached, software giants will go belly-up. But why RedHat will not be able to compete? Compete with what? If all proprietary companies will disappear, and only OSS companies remains, then the market actually increases, even with increasingly small revenues; the same effect that can be witnessed in some mobile data markets, with the reduction in price of SMS you see an increase in the number of messages sent, resulting in an increase in revenues.

“It is quite possible that the open source movement will ultimately result in a collapse of the industry, and that would not be a good thing.“

Still following the hypothetical theory that software pricing will go to zero (that, as I said, is not grounded in reality) here the author takes the previous considerations and uses a logical trick; he says that the proprietary companies will disappear, here he says that there will be a collapse of the industry (not of the “proprietary industry”). This way he collapses the concept of the software industry (that includes the proprietary and the non-proprietary actors) and conveniently avoids the non-proprietary part. Of course, this is still not grounded in anything logical. The conclusion is obvious: “that would not be a good thing”. Of course, this is another rhetoric form- by adding a “grounding” in something that is emotionally or ethically based, we introduce an external negative perception in the reader, strengthening what is still an hypothesis.

And then, the avoidance trap:

“I am sure that many open source advocates who are reading this are already irate, and perhaps even yelling that this Quinn guy doesn’t know what he is talking about. I am used to it by now; I get it all the time. It is, after all, much easier to simply believe that someone you disagree with is clueless rather than question your own beliefs“

This approach is so commonly used that is now beginning to show its age; use the fact that someone may be irate at reading the article to dismiss all critics as clueless people unable to question “beliefs”. The use of this word is another standard tactics, simply removing the idea that the personal position of an OSS adopter depends on illogic, faith-based assumptions; this, of course, would be difficult to defend in an academic environment, where we assume that researchers are not faith-based in their studies. So, this is an approach commonly used in online forum, blogs and such that are meant for a general audience.

“It is a mistake though to dismiss what I am saying here, or any of my other writings on computer software and open source.“

Of course, I am dismissing it for the content of what you write, not because of my “beliefs”; and I have not read anything else from you, so I am not dismissing what I have not read.

“The fact that I am a patent attorney undoubtedly makes many in the open source movement immediately think I simply don’t understand technology, and my writings that state computer software is not math have only caused mathematicians and computer scientists to believe I am a quack.“

This is totally unrelated to the previous arguments- who was talking of software patents anyway? We were talking about the role of OSS in terms of competition with the proprietary software market, and about potential effects to revenues.

“Unlike most patent attorneys, I do get it and that is probably why my writings can be so offensive to the true believers. I am not only a patent attorney, but I am an electrical engineer who specializes in computer technologies, including software and business method technologies. I write software code and whether you agree with me or not, telling me I simply don’t understand is not intellectually compelling.“

Of course, being part of a “class of people” like EE is in itself not qualifying in any way; any comment I made up to now would be equally applicable independently of the author; claiming to “get it” or implying that someone “don’t get it” because he works as a patent attorney is silly, and here the author falls in the same fallacy. By the way, I know some patent attorneys that perfectly “get it”, along with others that believe that open source software is made by fairies in the forest. As I said, being member of a class is in itself useless in deciding the truth of a statement.

“I do get it, and the reality is that open source software is taking us in a direction that should scare everyone.“

Here the author uses the fallacy of membership discussed before, and uses it as a authority power: “I do get it”. I am qualified, then I am saying the truth. And what I am saying is that OSS is dangerous, and the fact that anyone else (apart from O’Dowd, that believes that Linux will be infiltrated by terrorists) is not perceiving the problem is due to the fact that they are not looking with enough attention.

“Sun Microsystems is struggling, to say the least, and the reality is that they are always going to struggle because they are an open source company, which means that the only thing they can sell is service.“

Sun Microsystems is struggling for a long time now (unfortunately; I always loved their products). Personally I believe that the new CEO is doing quite a turnaround on the company, that has languished for a long time on a shrinking, highly lucrative market like SGI did in the past, but that is better left to financial analysts. Anyway their financial results were not that good even before the OSS turnaround imposed by Jonathan Schwartz, and so there is no real linking between the two part of the phrase (on the contrary, the OSS part is growing nicely, while the large scale enterprise server part is decreasing fast). It also introduces an additional error, that is the fact that being OSS means that you can sell only services. The author clearly has not read much on OSS business models, but he should not worry: I would be happy to send some papers on the subject.

“Whenever you sell time, earning potential is limited. There are only so many hours in the day, and only so much you can charge by the hour. When you have a product that can be replicated, whether it be a device, a piece of proprietary software or whatever, you have the ability to leverage, which simply doesn’t exist when you are selling yourself by the hour.“

Of course: this is the reality of consulting. This, however, does not stop companies like IBM Global Services, Accenture and friends to live off consulting, simply by asking very high prices for a day of a specialized consultant. Or, you can find groups like the 451 or RedMonk that are more efficient and targeted towards special markets.

“So there is a realistic ceiling on the revenue that can be earned by any open source company, and that ceiling is much lower than any proprietary software company.“

So, assuming that by-the-hour services is the only OSS business model possible, and that the price-per-hour cannot match that of large consulting firm, then there is a revenue ceiling that is lower than that of proprietary software companies. The fact that both parts of the phrase are unsustained by arguments makes the conclusion unproven.

“It is also an undeniable truth that the way many, if not most, service companies compete is by price. When service companies try and get you to switch over they will promise to provide the same or better service for a lower price.”

This should be a supporting argument for the fact that OSS companies charge a lower per-hour price of competing companies, and uses Sun as an example. Of course, it continues to be an unsupported argument, even considering the fact that the author probably never paid a receipt for a Sun consultant, or would have discovered that their pricing is in line with the rest of the market.

“The trouble with freeware is that there is no margin on free, and while open source solutions are not free, the race to asymptotically approach free is on, hence why I say the race to zero is in full swing.”

Now the author switches from OSS to “freeware”, to remind us that Open Source is, after all, free. Probably RMS would say at this point “free as in free speech, not free as in free beer”, but his ideas would be probably dismissed. The use of “free” here is made to create the appearance of a logical connection between “freeware” and open source; of course, the author acqnowledges that OSS is not free, but as part of the same “family” they are participating in the “asymptotically approach free… race to zero”. As stated before: in a perfect competition the race is not to zero, but to the marginal cost; so using “freeware” is a way to imply that this cost is zero as well, when the reality is that it is not zero (but lower than writing everything from scratch, thanks to the reuse opportunity).

And then we move to something completely different (as Monty Python would say):

“Unfortunately, many in the patent legal community are engaging in the race to zero as well. For example, there are patent attorneys and patent agents who advertise online claiming to be able to draft and file a complete patent application for under $3,000. One of the most common ads running provides patent applications for $2,800, and I have seen some agents advertise prices as low as $1,400 for a relatively simple mechanical invention. The race to zero is in full swing with respect to patent services aimed at independent inventors and start-up companies. It is also being pushed by major companies who want large law firms to provide patent services for fees ranging from $3,500 to $7,000 per application. This is forcing many large patent law firms to simply not offer patent drafting and prosecution services any longer. There are major law firms that are seeking to outsource such work, hoping to still keep the client for litigation purposes and to negotiate business deals.“

Dear writer, this is called “competition”. And as before, it is not a “race to zero”, as you will never find an attorney doing this kind of service for free, without any attachment; or if they do, they will probably go out of business, leaving the market.

“Does anyone really think that paying $1,400 for an allegedly complete patent application is a wise business decision? I can’t imagine that if you say that to yourself out loud it would sound like such a good idea.“

Well, IF the author can prove that application quality and price are correlated, then this becomes a decision based on economics principles (and depends on the hypothetical future value of the patent, measures of indirect value and so on). If the correlation is not strict, then any rational actor would simply seek the lowest possible price.

“Likewise, Fortune 500 companies that are pushing prices down and wanting to pay only $3,500 for a patent application can’t really expect to get much, if any, worthwhile protection. Do they? I suppose they do, but the reality is that they don’t. The reality is that when you are drafting a patent application you can ALWAYS make it better by spending more time. … But to think that you can force a patent attorney or agent to spend the same length of time working on a project whether you pay under $3,500, $7,000 or $10,000 is naïve. Everyone inherently knows this to be true, but somehow convinces themselves otherwise“

So, Fortune 500 companies are managed by morons, that don’t understand the value of spending more time. I suspect it is for a lack of culture, or a lack of perception of value; both can be cured by promotion and dissemination of information. Still, this does not applies to Open Source.

“As companies continue to look for the low cost solution, quality is sacrificed.“

Ah! Here’s the connection! As for patent applications, software has the same correlation: quality-price…

“Now I full well realize that much of the open source software is better than proprietary software, and I know that it can be much cheaper to rely on open source solutions than to enter into a license agreement for proprietary software.“

…but I can’t say it loud, thinks the author, or they will burn me alive. So, let’s change the subject again:

“But where is that going to lead us? Once mighty Sun Microsystems is hanging on for dear life, and is that who you want to be relying on to provide service for your customized open source solutions? What if Sun simply disappears?“

Can you trust a company like Sun, that by using OSS is destroying itself? Or are you thinking about using OSS, and take the risk of being such a dying corpse yourself? So, let’s make sure that the poor moron that thinks that OSS can save money understand the risks, by bringing another example: gyms!

“I remember years ago I joined a gym and purchased a yearly membership only to have the gym close less than 2 months later. A similar thing happened to my wife several years ago when she bought a membership to a fitness and well-being company who shall remain nameless. Eat better and get exercise counseling and support, what a deal! Of course, it was a deal only until the company filed for bankruptcy and left all its members high and dry. Luckily I put off joining myself otherwise we would have been out two memberships after less than 30 days.“

Of course, the parallel between gyms and software companies is not so strict; and is not related to OSS at all – examples abound of what happens, in all sectors. At least, with OSS, you have the source code, and you can do something yourself.

“With once mighty companies falling left and right do you really want to bet the IT future of your company or organization on an industry whose business model is the race to zero?”

So, dear author, the race is not to zero, and yes, I would bet it on open source, so at least I am free to continue to use your gym even after it has closed.

The new FLOSSMETRICS project liveliness parameters

Posted by cdaffara in OSS business models, OSS data, blog on April 2nd, 2009

While working on the final edition of our FLOSSMETRICS guide on OSS, I received the new automated estimation procedures from the other participants in the project and the QUALOSS people, namely Daniel Izquierdo. Santiago Dueñas and Jesus Gonzales Barahona from the Departamento de Sistemas Telemáticos y Computación (GSyC) of the Universidad Rey Juan Carlos. The new parameters will be included soon in the automated project page that is created in the FLOSSMETRICS database (here is an example for the Epiphany web browser); and will feature a very nice colour-coded scheme that provides an at-a-glance view of the risks or strengths of a project. A nice feature of FLOSSMETRICS is the fact that it provides information not only on code, but on ancillary metrics like mailing lists, committers participation, and so on, and all the tools, code, and databases are open source!

Now, on with the variables:

| ID | Measurement Procedure Idea | New Indicators |

| CM–SRA-1 | Retrieving the date of the first bug for each member of the community, we are able to know if the number of new member reporting bugs remains stable | Taking into account the slope of the resultant line (y=mx+b) while measuring the aggregated number and periods of one year: Green: if m > 0 Yellow: if m=0 Red: if m<0 Black if there are no new submitters for several periods |

| CM–SRA-2 | Retrieving the date of the first commit for each member of the community, we are able to know if the number of new member committing remains stable | Taking into account the slope of the resultant line (y=mx+b) while measuring the aggregated number and periods of one year: Green: if m > 0 Yellow: if m=0 Red: if m<0 Black if there are no new submitters for several periods |

| CM-SRA-3 | CVSAnalY: looking for the first commit of each detected committer in the SCM whose commit is not a code commit (for instance, ignoring source code extensions. MLS: Each new email address detected and its monthly evolution. Bicho: We measure monthly the first bug submitted by registered people. Retrieving the evolution of the first event in the community by a person and if it remains stable, can give an idea of how it evolves, and how many people are coming inside the community. | Taking into account the slope of the resultant line (y=mx+b) while measuring the aggregated number and periods of one year: Green: if m > 0 Yellow: if m=0 Red: if m<0 Black if there are no new submitters for several periods |

| CM-SRA-4 | Check the core group of developers (those with the 80% of the commits). Now check the first commit of each new member who starts working on the core group. Retrieving this information gives an estimator of how the core contributors is evolving. Thus, we can see if there is a natural regeneration of core developers. | Taking into account the slope of the resultant line (y=mx+b) while measuring the aggregated number and periods of one year: Green: if m > 0 Yellow: if m=0 Red: if m<0 Black if there are no new submitters for several periods |

| CM-SRA-5 | Core Team = people with the 80% of the commits. After this, any number of people who disappears from this core team is counted as one. Taking into account this metric we can estimate if there is a dramatic decrease in the number of core developers, and so, a risk in the regeneration. | Green: There are no members leaving the project Yellow: There are some people leaving the project, one or two each year Red: A high number of people leave the project. The evolution shows an increase or even a stable period. Black: The number of people leaving the project is extremely high. |

| CM-SRA-6 | Number of people who left the core team minus number of new members of the core team. Monthly analysis. | Green: The balance shows an increase in the number of people coming to the project Yellow: The balance is equal to 0 Red: The balance shows an increase in the number of people leaving the project Black: The balance shows a really high number of people leaving the project |

| CM-SRA-7 | Average age of people working on a project. This metric is focused on the average of years worked by each developer. With this approximation, we are able to know of members are approaching this limit and we can estimate future effort needs. | Green: The longevity is older than 3 years Yellow: The longevity is older than 2 years and younger than 3 years Red: The longevity is older than 1 year and younger than 2 years Black: The longevity is younger than 1 year |

| CM-SRA-8 | Evolution of people who contribute to the source code and reporting bugs. A way to retrieve this data is to analyze those committers and reporters with the same nickname. | Taking into account the slope of the resultant line (y=mx+b) while measuring the aggregated number and periods of one year: Green: if m > 0 Yellow: if m=0 Red: if m<0 Black if there are no new submitters for several periods |

| CM-SRA-9 | Same metric than above, but this is the sum of all of them, and not the evolution. General number. We can measure the size of a community. | Taking into account the slope of the resultant line (y=mx+b) while measuring the aggregated number and periods of one year: Green: if m > 0 Yellow: if m=0 Red: if m<0 Black if there are no new submitters for several periods |

| CM-IWA-1 | An event is defined as any kind of activity measurable from a community. Generally speaking, posts, commits or bug reports. Monthly analysis will provide a general view of the project and its tendency. | Taking into account the slope of the resultant line (y=mx+b) while measuring the aggregated number and periods of one year: Green: if m > 0 Yellow: if m=0 Red: if m<0 Black if there are no new submitters for several periods |

| CM-IWA-2 | Monthly analysis will provide a general view of the project. In this way an increase or decrease in the number of commits will show the tendency of the community | Taking into account the slope of the resultant line (y=mx+b) while measuring the aggregated number and periods of one year: Green: if m > 0 Yellow: if m=0 Red: if m<0 Black if there are no new submitters for several periods |

| CM-IWA-3 | Number of people working on old releases, out of total work on the project. We can determine how supported are the old releases for maintenance purposes. | Green: More than 10% Yellow: Between 5% and 10% Red: Between 0% and 5% Black: Nobody |

| CM-IWA-4 | Looking at the number of committers per each file. This metric shows the territoriality in a project. Generally speaking, most of the files are touched or handled by just one committers. It means that high levels of orphaning may be seen as a risk situation. If a developer leaves the project, her knowledge will disappear and all her files are totally unknown by the rest of the developers team. | Green: Less than 50% of the files are handled by just one committer Yellow: More than 50% of the files are handled by just one committer Red: More than 70% of the files are handled by just one committer Black: More than 90% of the files are handled by just one committer |

| CM-IWA-5 | Number of people working on the project, out of number of people working on the whole project and taking into account the whole set of activities to carry on. High number of SLOC, e-mails or bugs to be fixed per active developer may mean that they are overworked. In this case, the community is clearly busy and they need more people to help on it. | Green: Less than 30.000 Lines per committer and less than 25 bugs per committer Yellow: Between 30.000 and 50.000 lines per committer and between 25 and 75 bugs per committer. Red: Between 50.000 and 100.000 lines per committer and between 75 and 150 bugs per committer Black: More than 100.000 lines per committer and more than 150 bugs per committer |

| CM-IWA-6 | Relationship between committers and total number of lines or files. With this absolute number, we are able to check the number of lines per committer. Thus, just regarding to the source code, we can say if they need more resources on it. | Green: Less than 30.000 Lines per committer Yellow: Between 30.000 and 50.000 lines per committer Red: Between 50.000 and 100.000 lines per committer Black: More than 100.000 lines per committer |

| CM-IWA-7 | Knowledge of the current team about the whole source code, measured in number of files touched by all committers out of the total number of files. This metric gives an approximation of the number of files touched by the whole set of active committers. High percentages will show a high level of knowledge of the current developer team over the whole set of files. | Green: Less than 50 files Yellow: Between 50 and 200 files Red: Between 200 and 500 files Black: More than 500 files per committer |

(CVSanaly, Bicho, MLS are some of the tools that extract information from the various databases that we keep for every project; so for multidimensional data we extract variables from more than one source).

The evaluation becomes quite simple: if there is any red or black metric, you are looking at a high risk project, because there is a significant part of the code managed by a single, or a very small, group of people. We will estimate the number of yellow parameters that can be associated with a medium risk project by comparing our previous QSOS estimates with the new ones; it will be published directly in the guide.

As a side note: I am really grateful for the many researchers that are sending me their works within other open-source related EU projects; after all, we are all working for opennness ![]()

Random thoughts: TomTom, Alfresco

Posted by cdaffara in OSS business models, OSS data, blog on March 31st, 2009

Just a quick note on two relevant events in this beginning of week, first the TomTom settlement and the change in strategy of Alfresco (moving to an “open core” strategy).

As for TomTom: I am sorry for all the people that believed that the Dutch company could have been turned into a white knight of Linux, but it was clear from the start that the counter-suing was designed to create a level field for negotiation. There could be no CEO that would have fought the patent fight, understanding that in the eventuality of losing the amount of damages and remedial actions would have, effectively, killed the company. And you don’t know in advance what your chances are, and this is really one of the most dangerous aspects of patents. As for those that claimed that the FAT32 specification was effectively public, the reality is that courts rejected the patents on the original FAT implementation, but not its extensions; and that the “free to use” specification of FAT32 released by Microsoft are limited to the following areas:

“(e) Each of the license and the covenant not to sue described above shall not extend to your use of any portion of the Specification for any purpose other than (a) to create portions of an operating system (i) only as necessary to adapt such operating system so that it can directly interact with a firmware implementation of the Extensible Firmware Initiative Specification v. 1.0 (“EFI Specification”); (ii) only as necessary to emulate an implementation of the EFI Specification; and (b) to create firmware, applications, utilities and/or drivers that will be used and/or licensed for only the following purposes: (i) to install, repair and maintain hardware, firmware and portions of operating system software which are utilized in the boot process; (ii) to provide to an operating system runtime services that are specified in the EFI Specification; (iii) to diagnose and correct failures in the hardware, firmware or operating system software; (iv) to query for identification of a computer system (whether by serial numbers, asset tags, user or otherwise); (v) to perform inventory of a computer system; and (vi) to manufacture, install and setup any hardware, firmware or operating system software.”

So, hardly useable for anything within Linux. At the moment, probably the safest choice would be for embedded vendors to remove the FAT32-specific portions from the code, and use only the traditional 8.3 FAT allocation, eventually extending the use of filesystem-in-file strategy commonly used in games (like ID software’s PAKs).

As for Alfresco: first of all, I wish all the best for Alfresco and their product. It is always one of my favourite examples of successful commercial OSS system, and so I am happy to see that they are getting substantial increases in their turnover (including a nearly doubling of revenue year-over-year). On the other hand I understand perfectly the frustration that “some of the biggest enterprises in the world (and I mean Fortune 50 and even Fortune 10) are only using the open source version of the product”. It seems to me that the choice of what features should be available to enterprise customers vs. open source ones is a good initial choice, and I hope them every possible success. However, I am perplexed: if the OSS Alfresco is doing so well (doubling revenues!) is there really a need for a change in approach? And, given that RedHat is doing quite well, even with CentOS being used in many large scale companies, is it really necessary?

If the need to increase adoption was effectively so strong, I would probably have adopted a timed release for the bug fixes (effectively introducing a RHEL/Fedora like split), and spun off the plugins for connecting to the proprietary systems as a completely different offering; this way, the distinction between what is enterprise and what is open source would be clearer. Anyway: good luck, Alfresco! And continue to be my hero ![]()

I respectfully disagree.

Posted by cdaffara in OSS business models, OSS data, blog on March 25th, 2009

Microsoft has recently published a white paper on Microsoft and OSS, called “Participation in a world of choice”. It’s a nice 16-pages pdf, with kind words on the role of OSS in the modern IT landscape, the fact that “It is important to acknowledge that the relationship between open source and Microsoft has at times been characterized by strong emotions and harsh words” (some of which were from Microsofties themselves, like the infamous “cancer”), and that the future will be nice and warm and fuzzy. Despite the fact that – for probably the first time – a white paper contains a significant bibliography that includes academic papers, I have to say that I am not impressed by the content, that basically tries to reposition free software and open source in a context that is not entirely appropriate, and selectively presents a view of the market that is not in my opinion accurate.

(A note of warning: this post is not written out of “hate” of Microsoft. I am old enough to remember when IBM was the death empire (and its legal team was called “the nazguls” because they were unstoppable, fearless and devoid of human emotions), when Sun claimed that linux was a “bathub of code, … and sometimes what floats in it is not pleasant”, and at the same time I recognize the great advances that both companies made in recent years in open source. It would be my greatest pleasure to see Microsoft participate in OSS fully in the same way, but as it was for the companies I mentioned before, they have to prove themselves- and be slightly less schizophrenic in their message on OSS. End of note.)

So, I would like to point out a few things that I found in the paper:

- page 1: “… and increasing opportunities for developers to learn and create by combining community-oriented open source with traditional commercial approaches to software development.” First of all, not all open source is community oriented; here, Microsoft implies that all open source is developed in a community-oriented way (something that is not true, for example for dual-licensed software that has a much lower external participation rate, or for vendor-dominated consortia). Then, the use of “commercial” is wrong: free software and open source can be as commercial as software from the proprietary world. I would say that the copywriter here tried to suggest that OSS is “noncommercial” (something that our study , while the reality is that FLOSS in “nonproprietary”.

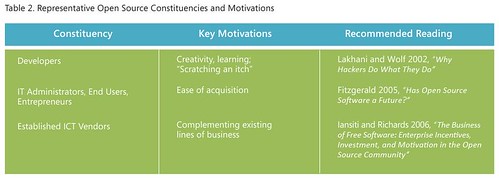

- Then we have the table in page 4:

What the present is a very limited view both of the constituencies, and the motivations for using OSS.There are many studies that present the reason for developers to participate in OSS; among them, ethical reasons, practical reasons (what is called here “scratching an itch”), self improvement, “signaling” (demonstrating capabilities in development to increase employment opportunities), and roughly 50% of the developers are paid to work on OSS. Assuming that transient reasons are the real motivations of OSS development provides a negative view (because as those personal interests may be short-lived, the software itself may be short-lived too).

- In the same table: the author places “IT Administrators, End Users, Entrepreneurs” in a single cathegory. Ok- this is not a research article, but even a novice would probably find differences among them. If the tags identify endogenous use, then having as a single advantage “ease of acquisition” is clearly a way to downplay the additional advantages of OSS. Among them, the reduced lock-in (that casually is never mentioned in the document), or reduced costs (as mentioned previously in my work on “OSS myths“, for example in the surveys by CIOinsight, or our work in the COSPA project). If the mention is for companies that use OSS inside their software (both for internal use or for commercialization) there are other demonstrations that OSS has substantial economic advantages. And where are the OSS companies? Those cannot be included in the last line, about “established ICT vendors”… They even mention themselves an example that does not fit in the table: “Apple shifted to what has been called an “embrace and layer” strategy for its consumer operating system by leveraging permissively licensed open source BSD code for functionality such as networking infrastructure, while focusing its commercial R&D on building a proprietary graphical user interface (GUI) “on top,” and licensing the resulting product as a whole under a traditional commercial license.” (In my classification, that would fit within the “R&D cost sharing”)

- Page 5: ” Another industry analyst firm, the 451 Group, identified more than 100 ICT companies who rely on OSS to generate a significant portion of their revenue. At the same time, it found “the majority of open source vendors utilize some form of commercial licensing to distribute, or generate revenue from open source software”. Of course! The error is the same already mentioned, that is the confusion between “proprietary” and “commercial”.

- Page 7: “OSS approaches tend to be relatively more successful when the end users of a technology are themselves developers, as opposed to nontechnical end users”. The phrase is incorrect, and arise from the identification of OSS developers as volunteers that “scratch an itch”. From a logical point of view, there are two errors: first of all, there are many technical users that are not developers (system administrators are a good example). In fact, the very high penetration of OSS in server environments is not strictly related to developer participation. Second, the assumption that OSS is inherently difficult to use (implied in the phrase) is easily dispelled by the great success of FireFox and OpenOffice (both of which require no “developer” in sight).

- Page 7: “Windows Server product strategy continues to focus on offering a product that IT administrators will choose over alternatives (including Linux), because it is highly manageable with readily available skills, supported by a wide range of third-party applications, and offers the lowest total cost of ownership (TCO).” This is marketing, not research- first of all, the TCO debate is still not solved in favor of Microsoft (and after reviewing the TCO numbers for COSPA, I suspect that that would not be an easy win for them). Then, it implies that OSS skills are not readily available (again, something that is unproven) and it implies that OSS alternatives have a limited range of third-party applications (look at RedHat certified applications list for a good counterexample).

- Page 8: “For developers, the entire .NET Framework is available as a reference source to enable them to debug against the source code”. And since it is not open source, this should probably not be mentioned here.

- Page 9: “One key, supporting principle is respect for the diverse—and continually evolving—ways that individuals and companies choose to build and market what they create. No efficient, effective technical solution should be precluded or advantaged because an individual, a vendor, or a development community has chosen a particular business model—whether based on software licensing, service and support, advertising, or, increasingly, some combination thereof.” This is aimed squarely at those governments that are trying to estabilish pro-OSS policies, and ignores the fact that in many cases the inherent market situation (with a de-facto monopoly) is not a balanced market in itself. Recently it was found that “Software tenders by European public administration often may not comply with EU regulations, illegally favouring proprietary applications”; so the advantage is at the moment squarely for proprietary software vendor, and the recent guidelines from the EU are designed to provide a more balanced market. My own suggestion is to evaluate the whole cost of an IT adoption using metrics that cover the full lifetime of an application; my favourite is the German WiBe model.

- Page 9: “A second key principle is a balance that preserves constructive competition and healthy incentives: when individuals and companies are rewarded for creative differentiation, customers benefit from a dynamic marketplace that offers more product choices. Incentives for commercial investment in new innovation should coexist and coevolve alongside practical mechanisms for sharing intellectual property (IP)—with the overarching focus on a dynamic industry that continues to bring great ideas to customers.” And this is for those that are asking for the abolition or the reduction in scope of software patents, and the invocation of open standards that are non-IPR encumbered. I already wrote in the past against software patents, and I believe to be not alone in claiming that the hypothetical advantage of software patents seems to pale in comparison to the extensive damage that it is causing to the industry. (And no- claiming that the thriving software ecosystem that we see now happens because of software patents should be rephrased in “the thriving software ecosystem that we see now happens despite of software patents”)

- Page 10: “We have long sought to contribute to the growth of an open ecosystem, whether through publicly documenting thousands of application programming interfaces (APIs)”. It took the European Commission, and a record fine for violation of EU monopoly laws, to abtain the release of crucial APIs…

- Page 10: “More than 500 commercial IP agreements with companies from a wide range of industries- including companies building their businesses around OSS”. Again: I would not claim that, after the substantial brouhaha in the Novell patent pact (considering that it does not covers things like OpenOffice…)

- Page 10: ” And we have stated broad openness to noncommercial OSS development through the Patent Pledge for Open Source Developers.” Nice- despite the fact that “noncommercial OSS” is an oxymoron, as placing additional redistribution limits make it non-OSS.

The paper ends with a very promising phrase: “We recognize that in the future, Microsoft ’s relationship with OSS may be punctuated by strong emotions and the possibility of interests that at times will be in conflict. But we are profoundly optimistic … will surface new opportunities for Microsoft and open source to “grow together” in purposeful and complementary ways.

I would be very happy to have Microsoft as a good OSS citizen, even with the recognition that their path may sometimes conflict (this is true also of other “fellows” like IBM or Sun, as well). But I would start with a more balanced introduction, or at least one that has not such a significant percentage of “hidden” ideas. Openness is before everything else in the mind; if your ideas are strong enough they will survive and thrive.

Another data point on OSS efficiency

Posted by cdaffara in OSS business models, OSS data on March 18th, 2009

I already wrote something in response to Savio Rodrigues post on the lack of differentiation in R&D expenditure between RedHat (“OSS”) and Microsoft and Tibco (“proprietary”). Savio found in the similar spending in R&D an indication that OSS companies are not implicitly more efficient, while I believe that the differences appear outside balance sheets, both in stronger offering and in competition efficiency, both not apparent in R&D spending.

A recent research from Venice University’s TEDIS seems to match at least part of my hipotesis:

“Infine, confrontando i singoli dati relativi alle sole imprese con fatturato inferiore ai 500.000 euro con la variabile relativa alle classi dimensionali delle aziende clienti (per numero di dipendenti), si può ipotizzare una correlazione tra l’utilizzo di software Open Source e la capacità di attrarre clienti di dimensioni relativamente più grandi. A parità di fatturato, insomma, le aziende “solo Open Source”, sembrano avere maggiori chances di ottenere commesse da aziende con oltre 50 dipendenti (quindi medio-grandi rispetto al nostro universo di riferimento).“

(my english translation: “Finally, comparing the individual data on firms with turnover of less than 500,000 euros with the variable on size classes of customers (by number of employees), one can hipotesize a correlation between the use of software Open Source and the ability to attract customers of relatively larger scale. At the same turnover, in other words, companies “Open Source only” seem to have more chances to obtain work orders from companies with more than 50 employees (ie medium – large compared to our universe of reference).”

This, given the relative similarity of other data (like revenue-per-employee of the cluster) provide at least an hint that OSS gives “leverage” in the kind of activities that a small company can create or propose to the market. As I wrote in my previous post: “In the smallest example (100000 lines of code, still substantial) the average staffing is reduced from more than 20 developers to slightly less than 9, bringing this project within reach even by small companies, and in my personal view it explains the exceptional take-up of OSS by new and innovative companies, that even before external sources of capital (like VCs) are capable of creating non-trivial projects with very limited resources.”

Estimating savings from OSS code reuse, or: where does the money comes from?

Posted by cdaffara in OSS business models, OSS data, Uncategorized on March 17th, 2009

We are approaching 100% of usage within other software, that is every software system contains some OSS code inside. Why? There is a perfectly sound reason, and this reason is related to a long standing tenet of software engineering: doing software takes time and money, and code needs to be maintained for a long time- adding additional costs on top. In one of the most widely known article in software engineering (“no silver bullet: essence and accidents of software engineering“), Frederick Brooks exposes some fundamental reasons behind the inherent difficulty of making software, especially large scale software systems. He also coined his law, the “no silver bullet law”:

There is no single development, in either technology or in management technique, that by itself promises even one order of magnitude improvement in productivity, in reliability, in simplicity.

Despite many trials, and many technologies (better languages, OOP, formal methods, automatic programming and many others..) the law has remained true until now. In the same article, however, Brooks marks some potential attacks on the inherent difficulty of making software:

- buy, don’t build (that is, if possible don’t code at all)

- requirement refining, rapid prototyping, incremental building

- great designers

It is quite easy to make a parallel with open source style development, that promotes the same ideas:

- reuse components and source code from other projects

- release early/release often (or allow anyone read access to CVS for making their own version)

- meritocracy (small group of respected core developers, and many smaller contributors)

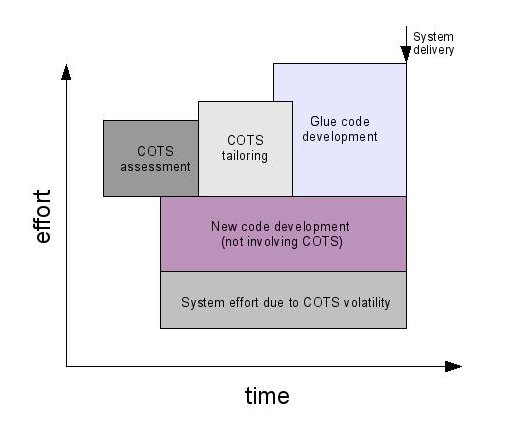

In the software engineering world the reuse of code coming from the “external” world is commonly called COTS, Commercial Off The Shelf, and has been studied for many years. Boehm and others created a model for mixed development that can be graphically presented as:

As can be seen in the image, there are costs that are related to the integration of COTS (in our case, OSS) within a newly developed product. These costs are related to the evaluation (and searching) of OSS, “tailoring” (the adaptation of the code for the project needs), and development of glue code (the layer of code between OSS modules and between OSS and internally developed code).

I would like to present some results based on the COCOMO II model, adapted to a model where a varying percentage of code is developed or reused from OSS. First of all, some assumptions:

- The average company cost of a developer is fixed at 25€ per hour. It should be a reasonable approximation of european costs (in particular, costs in mediterranean areas like Spain, France, Italy, Greece); we know that it is considerably lower than other estimates (especially US ones), but this way we provide a “lower bound” for savings instead of averages.

- The “tailoring” of code is performed on 15% of the OSS code; percentage comes from several separate projects, with estimates ranging from 5% for mature projects with structured and well-documented interfaces to 20% for complex, deeply-interlocked code like that found in embedded systems.

- Tailoring cost is higher than traditional coding; for this reason, the COCOMO complexity index is increased to 6 compared to new-code development.

- Volatility is based on our own model for cost estimation and data from literature on COTS (“Empirical observations on COTS software integration effort based on the initial COCOTS calibration database”, Abts C., Boehm B.W., Bailey Clark E.) and it can be approximate with an average effort equivalent to 1.5 to 2.5 full time person-year.

This is the result:

| Project size (lines of code) | % of OSS | total cost (Keuro) | Savings | duration (years) | avg. staffing |

| 100000 | 0 | 1703 | 0% | 1.7 | 20.5 |

| 100000 | 50 | 975 | 43% | 1.3 | 15.4 |

| 100000 | 75 | 487 | 71% | 0.9 | 8.6 |

| 1000000 | 0 | 22000 | 0% | 3.3 | 141.7 |

| 1000000 | 50 | 12061 | 45% | 2.6 | 103.2 |

| 1000000 | 75 | 3012 | 86% | 2 | 32 |

| 10000000 | 0 | 295955 | 0% | 7.5 | 818 |

| 10000000 | 50 | 160596 | 46% | 5.9 | 631.2 |

| 10000000 | 75 | 80845 | 73% | 3.8 | 421 |

In the case of 10Mlines of code, the saving is estimated at more than 210M€, that is consistent with previous estimates of savings by Nokia in reusing open source within Maemo. Even for the “small” project of 100000 lines, the savings are estimated at 1.2M€. Another interesting aspect is related to staffing and time: not only the use of OSS can reduce development time substantially, but it allows for a substantial reduction in the amount of staff necessary for the development. In the smallest example (100000 lines of code, still substantial) the average staffing is reduced from more than 20 developers to slightly less than 9, bringing this project within reach even by small companies, and in my personal view it explains the exceptional take-up of OSS by new and innovative companies, that even before external sources of capital (like VCs) are capable of creating non-trivial projects with very limited resources.

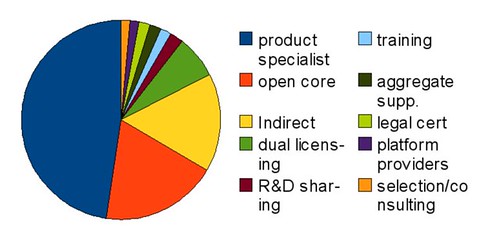

OSS-based business models: a revised study based on 218 companies

Posted by cdaffara in OSS business models, OSS data on March 16th, 2009

After the publication of our revised OSS business model taxonomy, we have finally finished the second survey from FLOSSMETRICS, that now covers 218 companies (again, excluding companies that have less than 30% of revenues coming from OSS, and excluding companies that sell a proprietary product based on OSS, as there are simply too many of them). Some companies are using more than one model (for example, many dual-licensing companies also sell services and support, and thus can be classified also as product specialists).

With the actual numbers:

| Model name | # companies |

| product specialist | 131 |

| open core | 52 |

| Indirect | 44 |

| dual licensing | 19 |

| R&D sharing | 6 |

| training | 5 |

| aggregate supp. | 5 |

| legal cert | 5 |

| platform providers | 4 |

| selection/consulting | 4 |

Some important considerations: product specialists are counted only when there is a demonstrable participation of the company into the project as “main committer”; otherwise, the number of specialists would be much greater, as some projects are the center of commercial support from many companies (a good example is OpenBravo or Zope). The distribution of revenue (approximate, as most companies are not publishing revenue data) seems to match that of average IT sector, with the vast majority of companies of small size (less than 5M$), around 10% are medium sized (5 to 20M$) and very few can be classified as “large”. Another observation is the fact that platform providers, while limited in number, tend to have a much larger revenue rate than both specialists or open core companies.

Overall there seems to be no significant difference in revenuse (comparing same-class companies) between product specialists compared to open core companies, but this is based on uncertain estimates of relative revenues, and should be taken as purely speculative. What seems to be constant is the reported increase in visibility and sales leads experienced by companies that adopted a pure open source model (be it dual licensing, specialists or based on indirect revenues); as before, it is possible to check this kind of increase only through web-based metrics (that are in many cases unreliable) and by indirect measurements like user participation in forums or dedicated conferences.

Another take on the financial value of open source

Posted by cdaffara in OSS business models, OSS data on March 13th, 2009

The “real” value of open source in financial terms has been one of my favourite arguments, and I had the opportunity to research in this area for a long time, thanks to our work for the customers for which we provide consulting on OSS business models. I recently found a new post on this by Bruno Von Rotz, with some preliminary conclusions like “total value of USD 100 to 150 billion.. I would assume that some of it comes from enterprises and large organizations, but this is probably max 20-30% of it.”

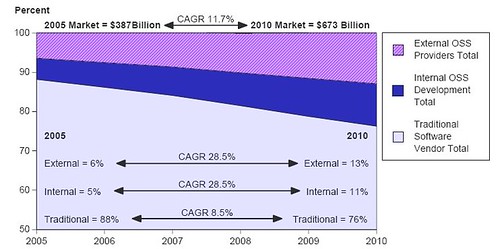

I would like to provide first of all a validation of the first part, and a comment on the second. As for the software market, Gartner published in 2006 a very well done study on OSS in the context of the overall software market, and among the various results there is one that I found quite interesting:

Considering the fact that some parallel data points (like results from the OECD estimates on software market) more or less confirm the predictions from Gartner, we can say that OSS has a financial value of 120B$ now, and will reach 150B$ in 2010, perfectly in line with the predictions from Bruno.

What I am not convinced is the calculation of the share 0f voluntary contributions Vs. company contributions. If Gartner data is accurate (and I believe that this is the case) we can expect that companies should contribute between 40% and 50% of value to a project; and this is somewhat consistent with projects like Linux or Eclipse where there is a large ecosystem, not only of adopters but of commercial companies working on top, and where company contributions are in that range. In this sense, I believe the 20%-30% percentage mentioned by Bruno to be too restrictive; the problem is that measuring code is not the only way to measure contributions. I use frequently this as an example:

“In the year 2000, fifty outside contributors to Open Cascade provided various kinds of assistance: transferring software to other systems (IRIX 64 bits, Alpha OSF), correcting defects (memory leaks…) and translating the tutorial into Spanish, etc. Currently, there are seventy active contributors and the objective is to reach one hundred. These outside contributions are significant. Open Cascade estimates that they represent about 20 % of the value of the software.”

Do these contributions appear as source code? No, exactly as localization efforts for OpenOffice or KDE do not appear in source code metrics. My belief is that the value of OSS right now is even much larger than 120B$, and that we have simply no way to measure this “hidden” value- but it’s there.

Our definitions of OSS-based business models

Posted by cdaffara in OSS business models, OSS data on March 13th, 2009

Two days ago, Matthew Aslett was so kind to comment on our new research on OSS business models; especially our new taxonomy, based on our latest extensions of the FLOSSMETRICS methodology and the increase in the number of surveyed companies. We both share the interest in having a clear, simple and usable set of definitions to avoid confusion when referring to specific business models; and he decided to publish the (previously private) set of definitions that were adopted in the CAOS report “Open source is not a business model“. As I would like to find a converging set of definitions, I will publish here a pre-release of our next edition of the OSS guide, that covers in more detail what Lampitt classify as “vendor licensing strategy”. My hope is to see if it is possible to find an agreed-to definition, that can be shared by researchers and experts. As already mentioned in my previous post, we introduced several changes compared to the previous edition:

- It does, for the first time, disaggregate what was originally called ITSC (Installation, training, support, consulting) because many successful companies are now specializing in a single activity. This is a significant change from 2006 (when we started collecting data on OSS models), when companies were performing in a more or less undifferentiated way all those activities. We believe that this “specialization” will continue with the enlargement of the commercial OSS market.

- We removed the “badgeware” category from the list. We found that some of the vendors that originally followed this model disappeared, and for those remaining protection from freeriding and overall model was more or less morphed into a “open core” or “split oss/commercial”. As the visibility clause can now be included in the GPLv3, I believe that the remaining few badgeware licenses will disappear quickly.

- As for our missing model (proprietary built on open) we found that basically the majority of products use OSS inside, so we are waiting to finish our second strand of research, on how to separate those products that are entirely OSS based from those that merely “use” OSS; our current idea is related to the “substitution principle”: is it possible to market the same product when all OSS components are substituted by non-OSS ones? Does it falls in the same market, or it becomes something radically different? This is a common theme, that tries to answer questions like “would it have been possible for Google to be based on proprietary software?”

Taking this into consideration, here is our new taxonomy:

- Dual licensing: the same software code distributed under the GPL and a commercial license. This model is mainly used by producers of developer-oriented tools and software, and works thanks to the strong coupling clause of the GPL, that requires derivative works or software directly linked to be covered under the same license. Companies not willing to release their own software under the GPL can buy a commercial license that is in a sense an exception to the binding clause; by those that value the “free as in speech” idea of free/libre software this is seen as a good compromise between helping those that abide to the GPL and receive the software for free (and make their software available as FLOSS) and benefiting through the commercial license for those that want to maintain the code proprietary. The downside of dual licensing is that external contributors must accept the same licensing regime, and this has been shown to reduce the volume of external contributions (that becomes mainly limited to bug fixes and small additions).

- Open Core (previously called split OSS/commercial): this model distinguish between a basic FLOSS software and a commercial version, based on the libre one but with the addition of proprietary plugins. Most companies adopt as license the Mozilla Public License, as it allows explicitly this form of intermixing, and allows for much greater participation from external contributions, as no acceptance of double licensing is required. The model has the intrinsic downside that the FLOSS product must be valuable to be attractive for the users, but must also be not complete enough to prevent competition with the commercial one. This balance is difficult to achieve and maintain over time; also, if the software is of large interest, developers may try to complete the missing functionality in a purely open source way, thus reducing the attractiveness of the commercial version.

- Product specialists: companies that created, or maintain a specific software project, and use a pure FLOSS license to distribute it. The main revenues are provided from services like training and consulting (the “ITSC” class) and follow the original “best code here” and “best knowledge here” of the original EUWG classification. It is based on the assumption, commonly held, that the most knowledgeable experts on a software are those that have developed it, and this way can provide services with a limited marketing effort, by leveraging the free redistribution of the code. The downside of the model is that there is a limited barrier of entry for potential competitors, as the only investment that is needed is in the acquisition of specific skills and expertise on the software itself.

- Platform providers: companies that provide selection, support, integration and services on a set of projects, collectively forming a tested and verified platform. In this sense, even Linux distributions were classified as platforms; the interesting observation is that those distributions are licensed for a significant part under pure FLOSS licenses to maximize external contributions, and leverage copyright protection to prevent outright copying but not “cloning” (the removal of copyrighted material like logos and trademark to create a new product). The main value proposition comes in the form of guaranteed quality, stability and reliability, and the certainty of support for business critical applications.

- Selection/consulting companies: companies in this class are not strictly developers, but provide consulting and selection/evaluation services on a wide range of project, in a way that is close to the analyst role. These companies tend to have very limited impact on the FLOSS communities, as the evaluation results and the evaluation process are usually a proprietary asset.

- Aggregate support providers: companies that provide a one-stop support on several separate OSS products, usually by directly employing developers or forwarding support requests to second-stage product specialists.

- Legal certification and consulting: these companies do not provide any specific code activity, but provide support in checking license compliance, sometimes also providing coverage and insurance for legal attacks; some companies employ tools for verify that code is not improperly reused across company boundaries or in an improper way.

- Training and documentation: companies that offer courses, online and physical training, additional documentation or manuals. This is usually offered as part of a support contract, but recently several large scale training center networks started offering OSS-specific courses.

- R&D cost sharing: A company or organization may need a new or improved version of a software package, and fund some consultant or software manufacturer to do the work. Later on, the resulting software is redistributed as open source to take advantage of the large pool of skilled developers who can debug and improve it. A good example is the Maemo platform, used by Nokia in its Mobile Internet Devices (like the N810); within Maemo, only 7.5% of the code is proprietary, with a reduction in costs estimated in 228M$ (and a reduction in time-to-market of one year). Another example is the Eclipse ecosystem, an integrated development environment (IDE) originally open sourced by IBM and later managed by the Eclipse Foundation. Many companies adopted Eclipse as a basis for their own product, and this way reduced the overall cost of creating a software product that provides in some way developer-oriented functionalities. There is a large number of companies, universities and individual that participate in the Eclipse ecosystem; as an example:

As recently measured, IBM contributes for around 46% of the project, with individuals accounting for 25%, and a large number of companies like Oracle, Borland, Actuate and many others with percentages that go from 1 to 7%. This is similar to the results obtained from analysis of the Linux kernel, and show that when there is an healthy and large ecosystem the shared work reduces engineering cost significantly; Gosh estimates that it is possible to obtain savings in terms of software research and development of 36% through the use of FLOSS; this is, in itself, the largest actual “market” for FLOSS, as demonstrated by the fact that the majority of developers are using at least some open source software within their own code.

As recently measured, IBM contributes for around 46% of the project, with individuals accounting for 25%, and a large number of companies like Oracle, Borland, Actuate and many others with percentages that go from 1 to 7%. This is similar to the results obtained from analysis of the Linux kernel, and show that when there is an healthy and large ecosystem the shared work reduces engineering cost significantly; Gosh estimates that it is possible to obtain savings in terms of software research and development of 36% through the use of FLOSS; this is, in itself, the largest actual “market” for FLOSS, as demonstrated by the fact that the majority of developers are using at least some open source software within their own code. - Indirect revenues: A company may decide to fund open source software projects if those projects can create a significant revenue source for related products, not directly connected with source code or software. One of the most common cases is the writing of software needed to run hardware, for instance, operating system drivers for specific hardware. In fact, many hardware manufacturers are already distributing gratis software drivers. Some of them are already distributing some of their drivers (specially those for the Linux kernel) as open source software.

The loss-leader is a traditional commercial model, common also outside of the world of software; in this model, effort is invested in an open source project to create or extend another market under different conditions. For example, hardware vendors invest in the development of software drivers for open source operating systems (like Linux) to extend the market of the hardware itself. Other ancillary models are for example those of the Mozilla foundation, that obtains a non trivial amount of money from a search engine partnership with Google (an estimated 72M$ in 2006), while SourceForge/OSTG receives the majority of revenues from ecommerce sales of the affiliate ThinkGeek site.

At the moment there is no “significant” model, with companies more or less adopting and changing model depending on the specific market or the shifting costs. For example, during the last few years a large number of companies shifted from an “open core” model to a pure “product specialist” one to leverage the external community of contributors. Many researchers are trying to identify whether there is a more “efficient” model among all those surveyed; what we found is that the most probable future outcome will be a continuous shift across model, with a long-term consolidation of development consortia (like Symbian and Eclipse) that provide strong legal infrastructure and development advantages, and product specialists that provide vertical offerings for specific markets.